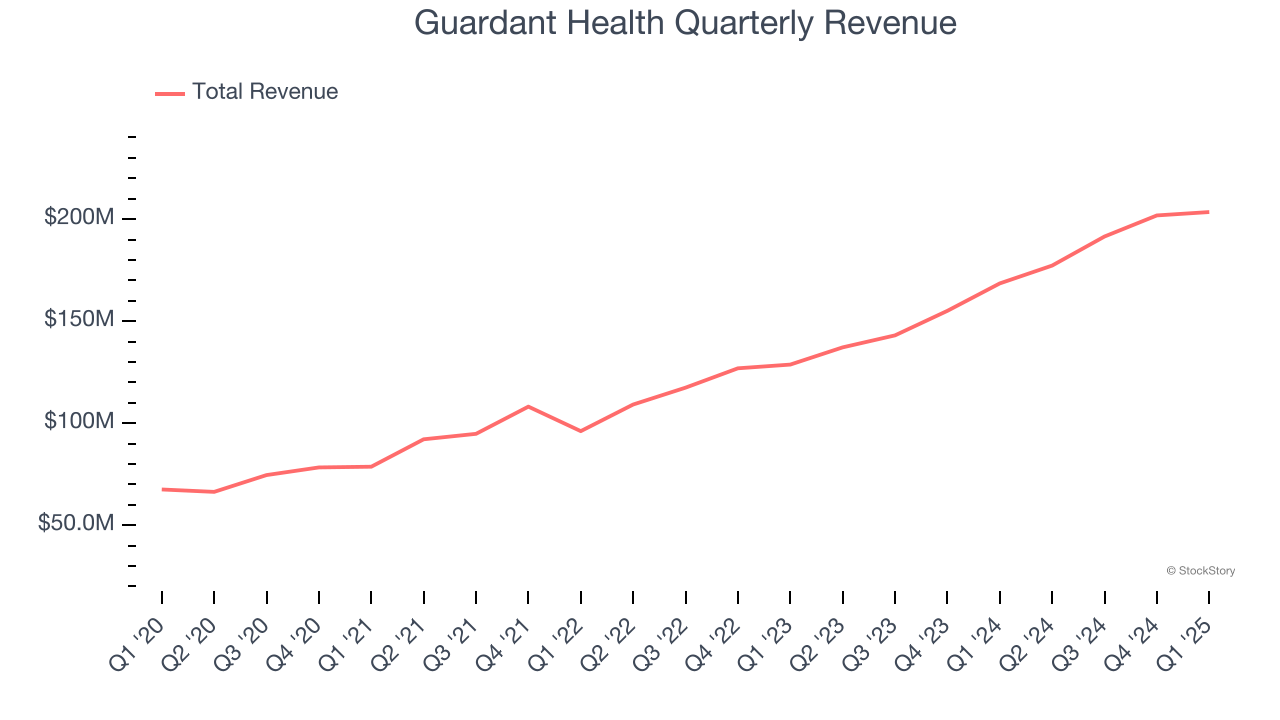

Diagnostics company Guardant Health (NASDAQ:GH) reported Q1 CY2025 results topping the market’s revenue expectations, with sales up 20.8% year on year to $203.5 million. The company’s full-year revenue guidance of $885 million at the midpoint came in 3.2% above analysts’ estimates. Its non-GAAP loss of $0.49 per share was 17% above analysts’ consensus estimates.

Is now the time to buy Guardant Health? Find out by accessing our full research report, it’s free.

Guardant Health (GH) Q1 CY2025 Highlights:

- Revenue: $203.5 million vs analyst estimates of $190.3 million (20.8% year-on-year growth, 6.9% beat)

- Adjusted EPS: -$0.49 vs analyst estimates of -$0.59 (17% beat)

- Adjusted EBITDA: -$58.54 million vs analyst estimates of -$78.16 million (-28.8% margin, 25.1% beat)

- The company lifted its revenue guidance for the full year to $885 million at the midpoint from $855 million, a 3.5% increase

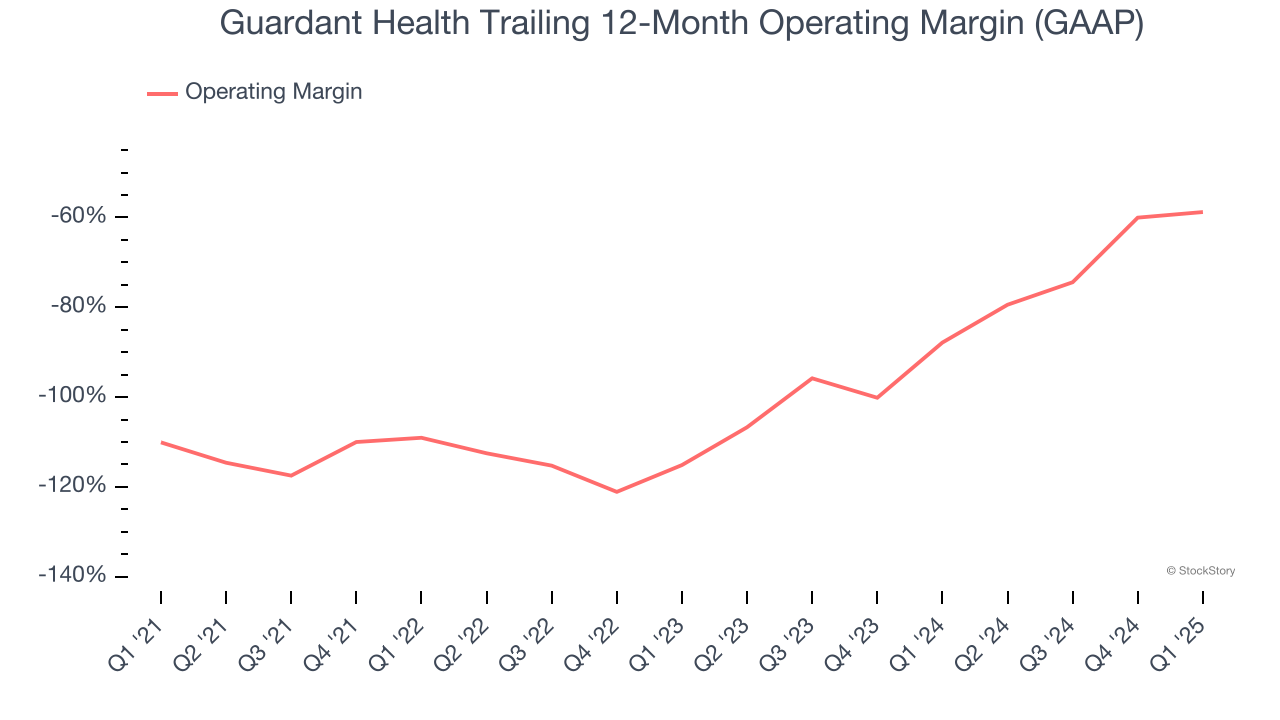

- Operating Margin: -54.6%, up from -59.2% in the same quarter last year

- Free Cash Flow was -$67.15 million compared to -$37.22 million in the same quarter last year

- Sales Volumes rose 25.8% year on year (19.9% in the same quarter last year)

- Market Capitalization: $6.11 billion

Company Overview

Pioneering the field of "liquid biopsy" with technology that can identify cancer-specific genetic mutations from a simple blood draw, Guardant Health (NASDAQ:GH) develops blood tests that detect and monitor cancer by analyzing tumor DNA in the bloodstream, helping doctors make treatment decisions without invasive biopsies.

Testing & Diagnostics Services

The testing and diagnostics services industry plays a crucial role in disease detection, monitoring, and prevention, serving hospitals, clinics, and individual consumers. This sector benefits from stable demand, driven by an aging population, increased prevalence of chronic diseases, and growing awareness of preventive healthcare. Recurring revenue streams come from routine screenings, lab tests, and diagnostic imaging, with reimbursement from Medicare, Medicaid, private insurance, and out-of-pocket payments. However, the industry faces challenges such as pricing pressures, regulatory compliance, and the need for continuous investment in new testing technologies. Looking ahead, industry tailwinds include the expansion of personalized medicine, increased adoption of at-home and rapid diagnostic tests, and advancements in AI-driven diagnostics that enhance accuracy and efficiency. However, headwinds such as reimbursement uncertainties, competition from decentralized testing solutions, and regulatory scrutiny over test validity and cost-effectiveness may impact profitability. Adapting to evolving healthcare models and integrating automation will be key for sustaining growth and maintaining operational efficiency.

Sales Growth

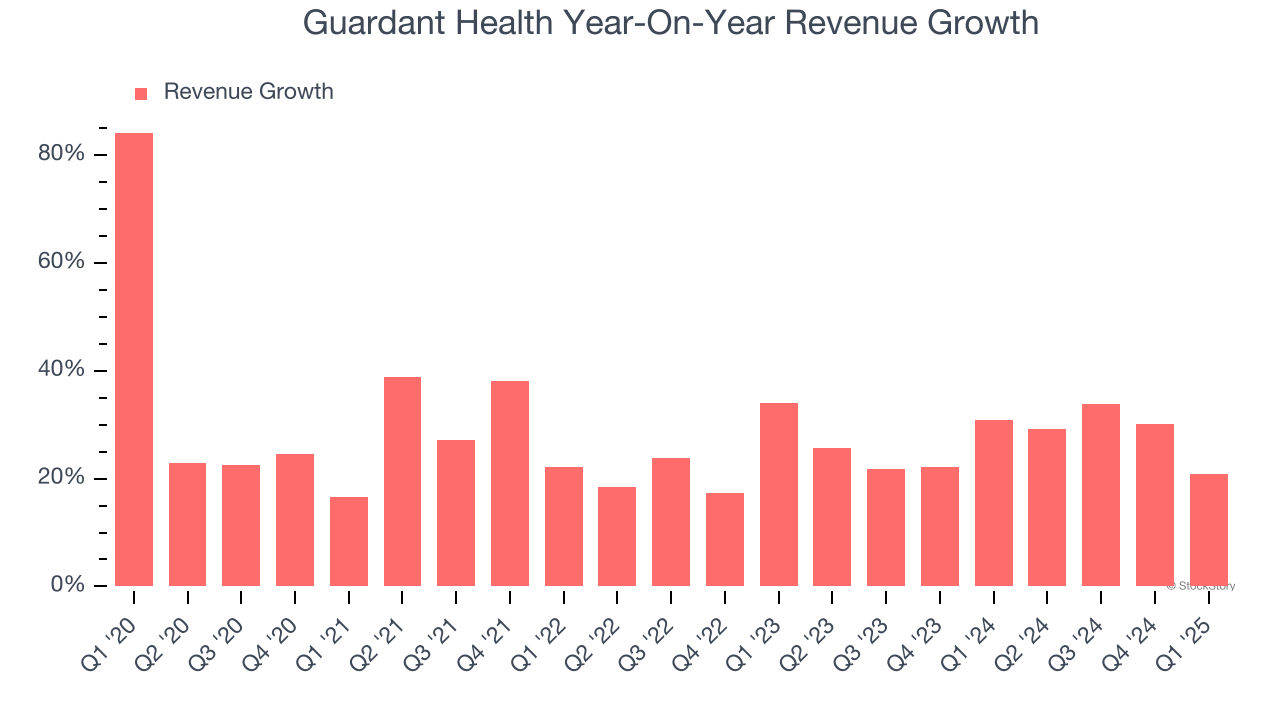

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Guardant Health’s sales grew at an exceptional 25.8% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Guardant Health’s annualized revenue growth of 26.7% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

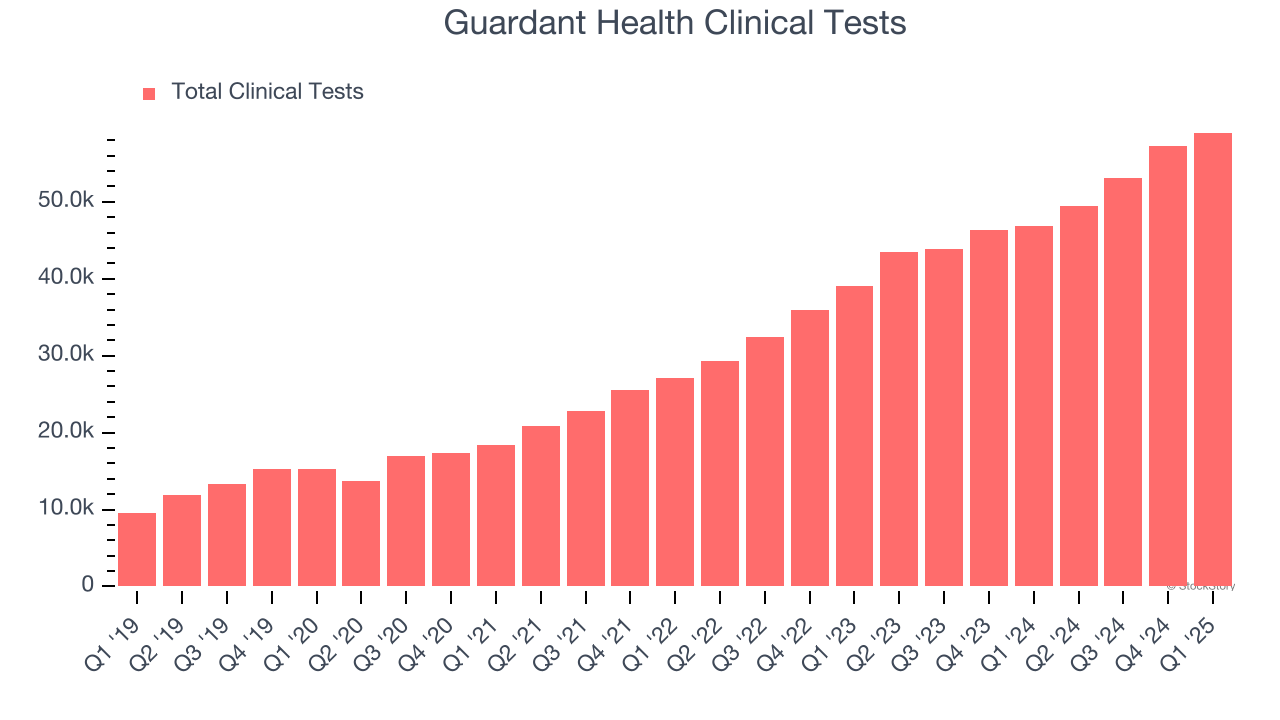

Guardant Health also reports its number of clinical tests, which reached 59,000 in the latest quarter. Over the last two years, Guardant Health’s clinical tests averaged 27.1% year-on-year growth. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, Guardant Health reported robust year-on-year revenue growth of 20.8%, and its $203.5 million of revenue topped Wall Street estimates by 6.9%.

Looking ahead, sell-side analysts expect revenue to grow 16.3% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and suggests the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Guardant Health’s high expenses have contributed to an average operating margin of negative 90% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Guardant Health’s operating margin rose by 51.3 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 56.3 percentage points on a two-year basis. These data points are very encouraging and shows momentum is on its side.

In Q1, Guardant Health generated a negative 54.6% operating margin. The company's consistent lack of profits raise a flag.

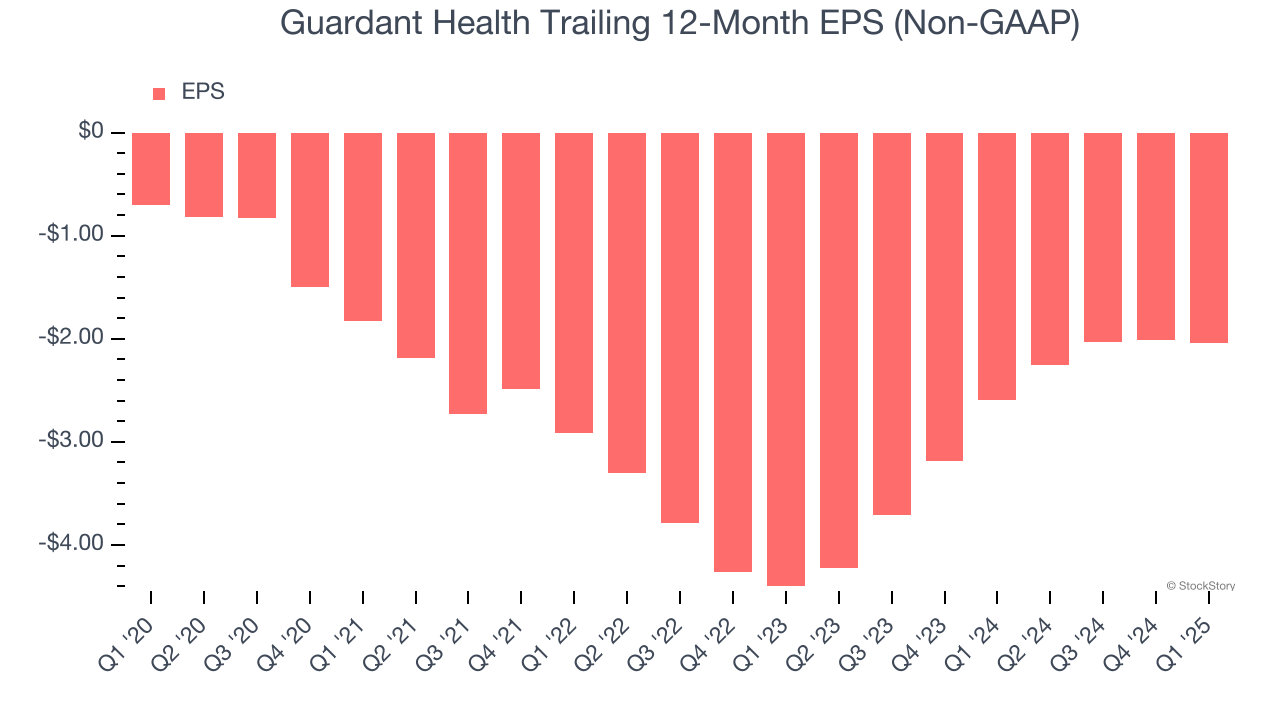

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Guardant Health’s earnings losses deepened over the last five years as its EPS dropped 23.7% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

In Q1, Guardant Health reported EPS at negative $0.49, down from negative $0.46 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Guardant Health to perform poorly. Analysts forecast its full-year EPS of negative $2.04 will tumble to negative $2.06.

Key Takeaways from Guardant Health’s Q1 Results

We were impressed by how significantly Guardant Health blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. We were also glad it raised its full-year revenue guidance given the strong performance in clinical test volumes. Zooming out, we think this was a solid quarter. The stock traded up 6.8% to $50.40 immediately after reporting.

Guardant Health had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.